Peeling the ‘Value onion’

I have worked with services and sales throughout my career, both technically, operationally, and commercially. My first job after graduating from a technical university was with Ericsson's services business organisation in Stockholm, Sweden. Here I first got introduced to the concepts of ‘customer value’ and ‘value based selling’.

They were in the process of establishing a new services business unit with high growth expectations for the company. The services portfolio was designed to complement the telecommunications infrastructure offering with traditional network ‘Build, Operate and Maintain’ services, as well as a Professional Services portfolio that included stand-alone advisory consulting services.

In this services-growth environment, there was a lot of activity and ambition around establishing sales, delivery, and business development strategies for the telecom customer base. I was fortunate to be part of a multinational organisation that was constantly brainstorming, debating, and creating value through its services offering.

However, I found the concept of ‘customer value’ to be vague for quite some time, even though the term was frequently used on all organisational levels. I felt that I needed to understand it better.

My thoughts on ‘Creating value’

It was not until work progressed by complementing marketing and sales material and value argumentation with customer-oriented business case exercises that things started to become clear for me. I found that business cases had a powerful effect in both the design phase, working backwards (as in ‘peeling the onion’), defining and quantifying all given parameters in terms of financial numbers, and in the concluding phase, when summarising the customer value as increased profit, reduced cost or shorter time to revenue etc.

To me, the business case approach made the value argumentation ‘non-controversial, easy to understand and easy to communicate’. As we had assumed certain variables, we asked clients to validate these themselves during sales engagements and by doing so, we introduced a ‘consultative sales tactics’ which had the effect that customers started feeling ownership and confirming the value definition. This is an effective way of having your (potential) customer validate value - which in sales is a clear ‘buying signal’.

I have since that time, until today, used this tactic of letting the client participate and shape the final value definition in several different ways and environments.

““The value is always in the eye of the beholder.

What is worthless to one person may be

very important to someone else.””

I believe the same applies to ‘value’ in the context of business, which is why it is a controversial ‘product’ for any organisation to design, market, and sell to a wider audience. Many companies are successful in doing so, but it requires significant investments in skill, effort, and maintenance to keep it relevant for the customer, for whom the perception of value also changes over time, making it a continuously moving (investment intensive) target.

““There are two main types of value creation:

financial and non-financial. Financial value is based on

tangible measures such as revenue and profits.

Non-financial value is based on intangible value””

My strategy as an external supporting resource is to prioritise financial value, as I believe it in turn increases an organisation's own ability generating non-financial value. However, sometimes these cannot be separated, which is why parallel processing becomes important by identifying the low-hanging fruit first, resulting in a faster cash conversion for the client.

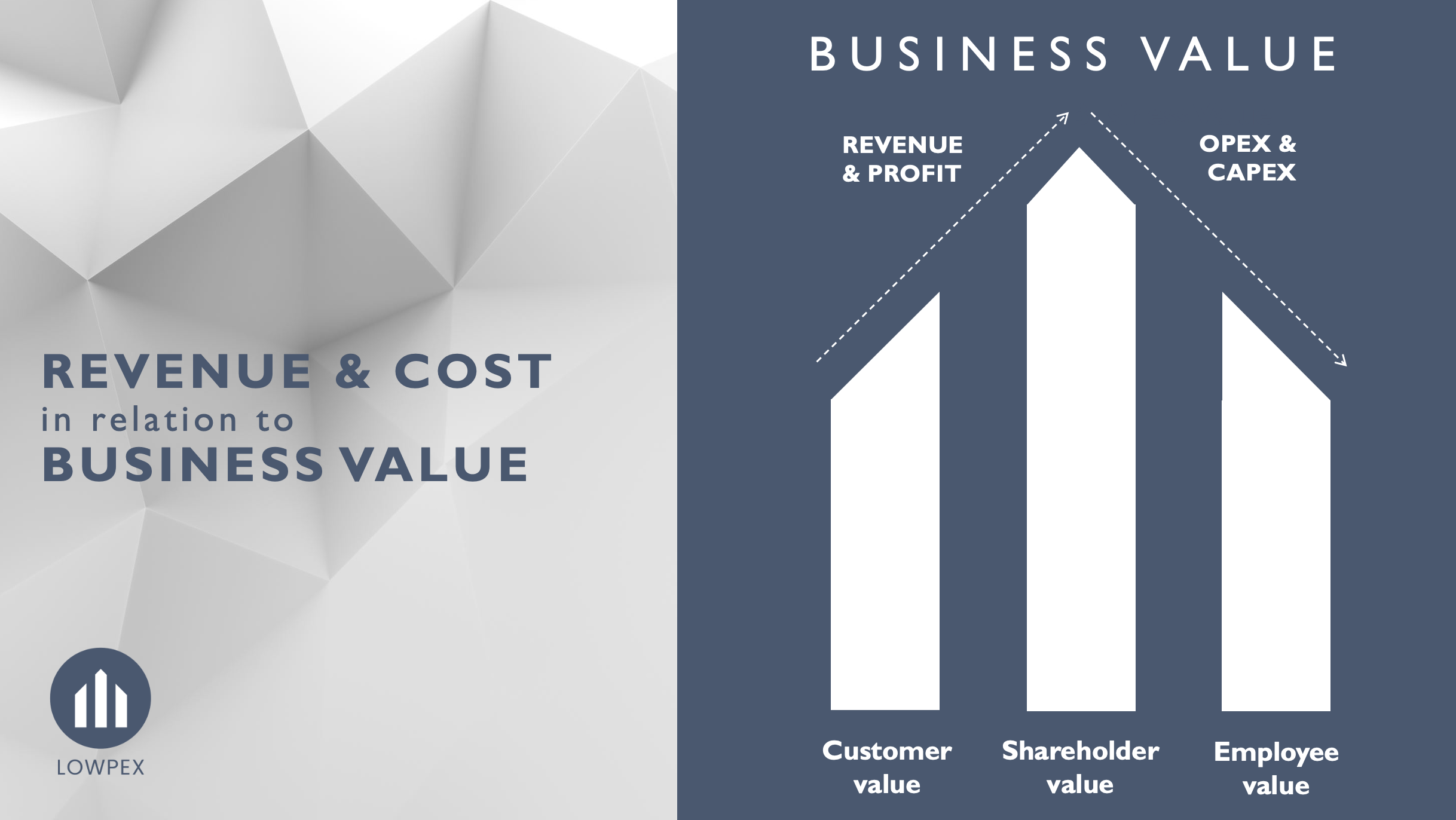

The three main ‘Value dimensions’

When analysing how to generate business value, there are three main underlying dimensions to consider:

Customer value - Innovative and high quality products & services

Shareholder value - Return on Investment

Employee value - Compensation & Benefits, Employee growth & retention

From a financial-value perspective, the one thing these three value dimensions have in common is they require continuous investment:

Customer value - Investment in R&D, Product management, Operational excellence

Shareholder value - Investment yield for shareholders & investors

Employee value - Investment in human capital, work environment, compensation and benefits

If you exclude external investments (such as raising capital by issuing shares, bonds or taking on debt etc), the main method of generating (or 'freeing up') internal investment is simply by 'keeping cost in line with revenue' to ensure profit. So, perhaps unsurprisingly, maximising financial business value boils down to maximising revenue and minimising costs, which in turn will increase the ability creating non-financial value.

Maximising revenue is probably the most widely explored aspect of business, and some even view ‘Sales’ as an art form. Does this mean that the practice of minimising cost is also considered an art form?

“A simple search on Linked-In generated

+25 000 results for ‘Chief Revenue Officer’ versus

9 (nine) results for ‘Chief Cost Officer’”

With the above, I am not stating that cost responsibility is not established within most organisations. It is, for example, often a part of the Finance, Procurement, Operations, or Supply Chain responsibilities within companies. Additionally, any manager accountable for a Profit or P&L business target also has a cost responsibility (directly or indirectly). The exception is when a company financially is underperforming and not meeting set expectations, in which case cost optimisation may temporarily take precedence over revenue.

The ‘organisational Revenue versus Cost discrepancy’

I do however believe that, generally speaking, there is a discrepancy between the organisational authority, accountability, and proactivity allocated to ‘revenue & profit’ versus ‘cost’ considering the significance that cost has on a company's net business value.

I see a similar pattern in public society where government representatives and politicians have endless debates about the national budget, for example, how much to invest in the various areas of society, but there is relatively speaking very little debate about how wisely the budget and public tax funds are spent from a cost-effectiveness point of view.

It seems that the cost responsibility in that regard is delegated to the underlying organisations accountable for the respective services in society and then we are back to the ‘organisational cost versus revenue & profit discrepancy’ I described above (although tax funds usually are also governed by a public procurement act).

““If you know how to address ‘Cost’ it is your

fast-track opportunity to value creation””

This is why I see ‘cost optimisation’ as an area of opportunity as it opposed to 'direct value creation', is more accessible to address and also 'non-controversial, easy to understand & easy to communicate'. Depending on a company’s profit margin 1 dollar saved is worth 2-10 dollars of revenue. This makes it an effective tool for creating tangible business value for basically any and all organisations out there.

Furthermore, ‘Customer value creation’ only (directly) drives one of three value dimensions, whereas ‘cost optimisation’ generates end-to-end business value for a company (which I find interesting as ‘cost’ many times is regarded as an ‘indirect’ approach to creating value).

“‘Value investing’ is an investment strategy that involves buying stocks that appear underpriced relative to their intrinsic value.”

Another example where I have come across the 'value' terminology is via my personal interest in the financial stock market and investment strategies. Having recovered from the financial investment hangover I also suffered after the millennial IT-bubble, I started searching for a wiser investment strategy and found that 'Value investing' or 'Value stocks' is a very popular concept. But also here I found that the term 'value' was ambiguous and vaguely defined.

As I wanted to understand the concept of 'value investing' better, I ended up finding (one out of many strategies out there) 'the quantitative investment strategy: Trending Value Composite' (by James O'Shaughnessy) which is based on several financial performance indicators with individual and defined purpose (the interested reader can check out Valuesignals). The model has been 'backtested' decades back and is therefore a (historically) proven, objective, and transparent way of qualifying and investing in value stocks.

With this strategy, I think that finding 'Value Stocks' became 'non-controversial, easy to understand & easy to communicate' which is the point I wanted to emphasise (so as not to be seen as investment advice).

- Josef K. Lindgren